How Interest Rates Are Shaping The House Market in Atlanta

Tips for Sellers Todd Kroupa March 6, 2025

Tips for Sellers Todd Kroupa March 6, 2025

Interest rates are one of the most influential factors affecting the housing market. Whether you're a first-time homebuyer, a homeowner, a seasoned investor, or simply keeping an eye on real estate trends, understanding how interest rates impact home prices, mortgage affordability, and market demand is key to making informed real estate decisions.

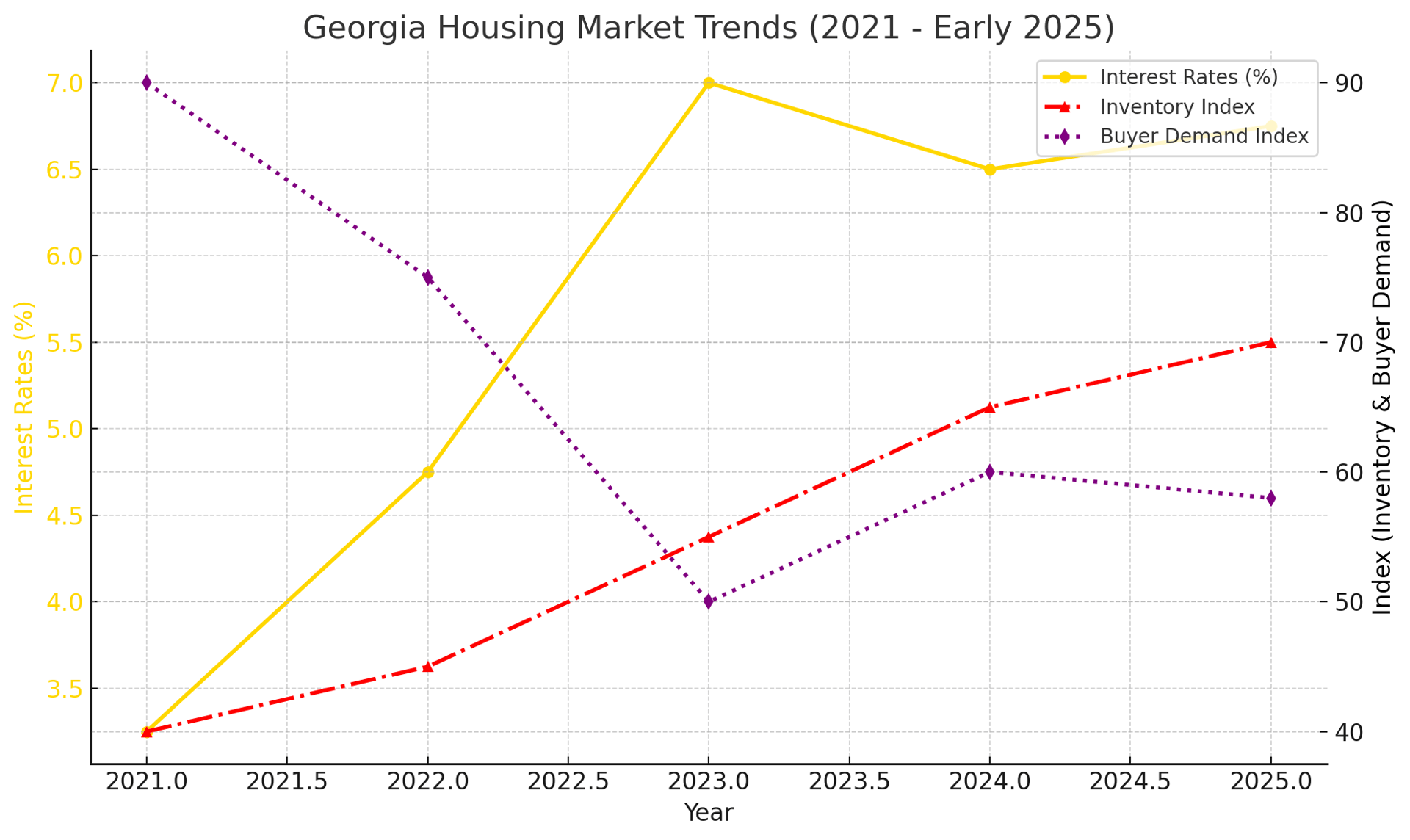

In Alpharetta, Milton, and North Metro Atlanta, the impact of mortgage rate changes was particularly pronounced in 2023 and 2024. With interest rates now hovering around 6.5%-7% as of Feb/March 2025, homebuyers and sellers are adjusting their strategies. In this post, we’ll explore how changing interest rates shape the housing market and what this means for buyers, sellers, and investors in the Atlanta area.

How Interest Rates Impact Mortgage Affordability

The Link Between Interest Rates and Monthly Payments

Mortgage interest rates directly influence how much homebuyers can afford. When rates are low, buyers can secure larger loans while keeping their monthly payments manageable. However, as interest rates rise, borrowing costs increase, reducing purchasing power.

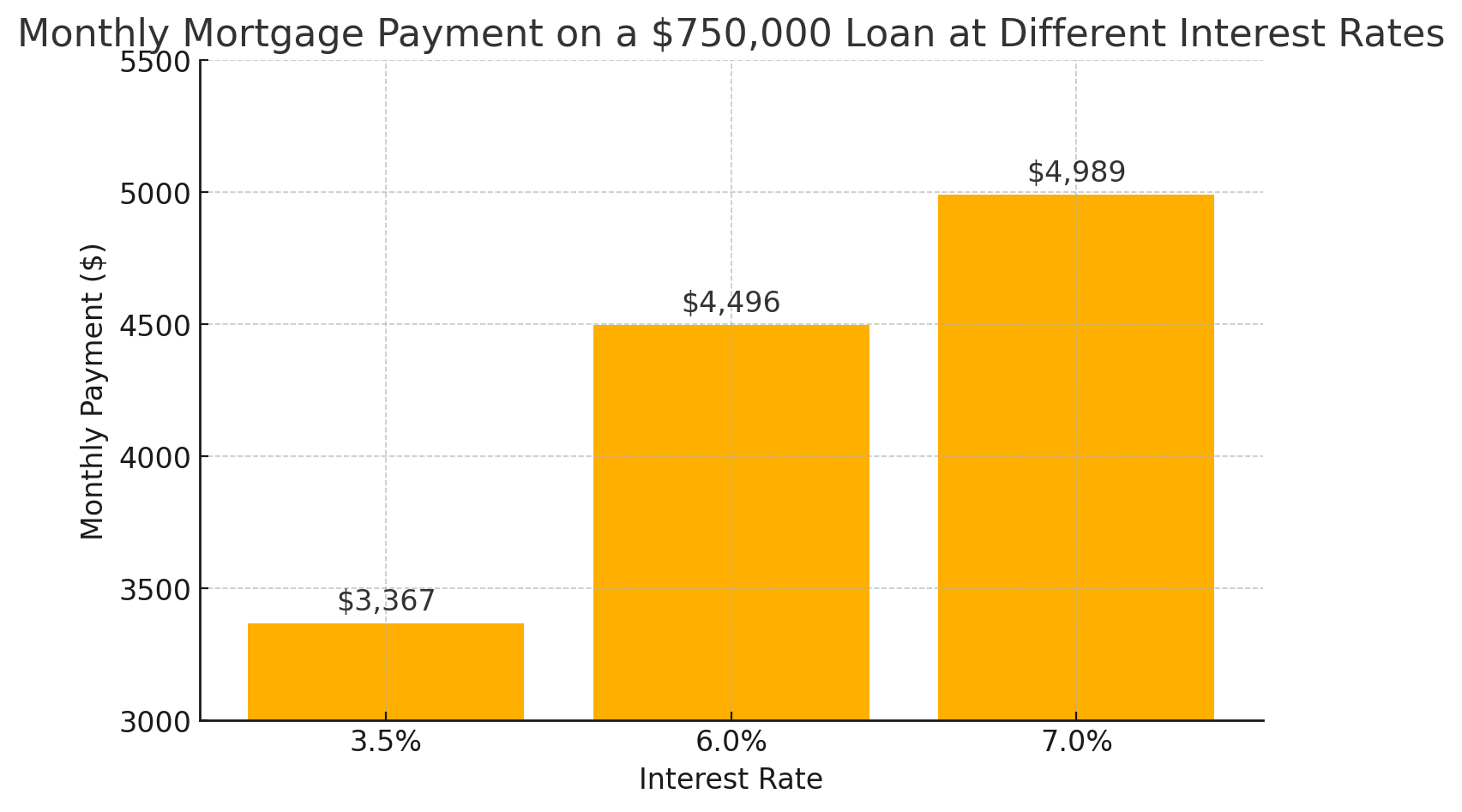

To put this into perspective, below is a comparison of monthly principal and interest payments on a $750,000 mortgage at different interest rates (excluding taxes and insurance):

Monthly Payment Differences:

This increase in mortgage costs means that buyers may need to adjust their home budgets or look at different financing options. Even a 1% change in interest rates adds hundreds of dollars to a monthly payment, making homeownership less accessible for some buyers.

Refinancing Opportunities

When mortgage rates were lower, many homeowners chose to refinance to lower their payments or shorten their loan terms. In contrast, when rates rose—as they did in 2024—refinancing became less attractive. Homeowners who secured 3-4% mortgage rates in previous years opted to stay put rather than take on new loans at higher rates.

However, if interest rates decrease later in 2025 or 2026, we may see a renewed wave of high buyer demand activity in the Atlanta real estate market.

The Effect of Interest Rates on Home Prices

Demand and Affordability

Interest rates play a key role in housing demand. Lower rates typically encourage buying activity, leading to higher home prices as demand increases. Conversely, rising interest rates can slow demand, resulting in longer listing times and potential price adjustments.

In Alpharetta and Milton, where home prices are already high, rising interest rates softened demand in some price points. However, limited inventory continued to support stable home values, preventing significant recession-like price declines.

Supply and Market Dynamics

Higher interest rates didn’t just affect buyers—they also impacted sellers. Homeowners who had low mortgage rates were reluctant to sell, knowing they would have to take on a higher-rate mortgage for their next home. This contributed to low inventory levels in North Metro Atlanta, which helped keep prices from dropping despite a slowdown in buyer demand.

If rates remain elevated, new construction homes and renovated, move-in-ready properties may become more attractive as buyers look for homes where they won’t need to make major upgrades or refinance quickly.

Interest Rates and Housing Market Trends

Buyer Sentiment and Market Cycles

When rates were low, buyer confidence was high, leading to competitive markets and multiple-offer situations. In contrast, rising rates cooled the market, to a more neutral state leading to:

Practical Tips for Buyers and Sellers in a Changing Rate Environment

For Homebuyers in Today’s Market:

For Sellers in Today’s Market:

Conclusion: What’s Next for the Atlanta Housing Market?

Interest rates remain a key factor shaping the housing market in Alpharetta, Milton, and North Metro Atlanta. While rising rates have affected affordability, low inventory levels have helped keep home prices stable.

If you’re considering buying or selling in 2025, staying informed about mortgage trends and local market conditions can help you make the right move.

Have questions about how interest rates are impacting your real estate goals?

Reach out to Todd Kroupa and The Kroupa Team for expert guidance on navigating the current real estate market in Alpharetta, Milton, and North Metro Atlanta!

Smart Improvements to Help You Get the Most From Your Sale.

What To Look For When Finding Your Perfect Space.

Creating a Space That Feels Both Personal and Put-Together.

Selling a home or property with the Kroupa Team assures you the highest professionalism and real estate consultation available in North Metro Atlanta communities. With over 18 years of experience marketing and selling luxury homes, equestrian properties, and residential real estate, you will receive unsurpassed customer service and guidance from listing to sell.